Best Insurance Technology for the USA Market in 2026

2026 is the year insurance goes digital, data‑driven, and deeply personalized. As insurers compete for customers and operational efficiency, technology is no longer optional — it’s strategic. From AI and automation to IoT and embedded insurance, today’s tech stack is transforming everything from pricing and underwriting to claims and customer engagement.

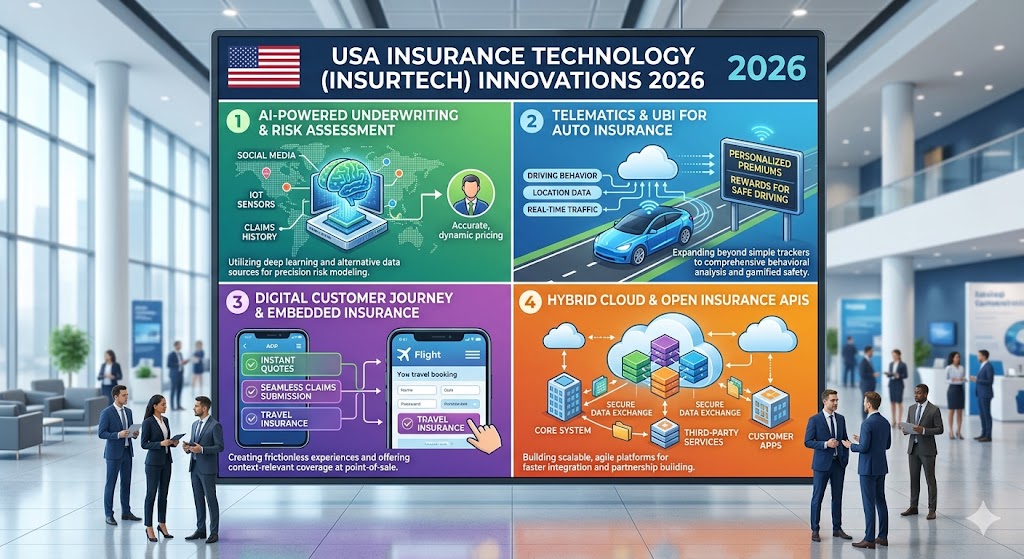

1. AI and Machine Learning Are the New Core

Artificial intelligence has moved far beyond pilot projects. In 2026, U.S. insurers are embedding AI throughout core systems — underwriting, claims, pricing, fraud detection, and customer experience. Instead of sporadic experimentation, AI now drives real business outcomes, optimizing risk decisions in real time and boosting operational efficiency.

Why it matters:

Reduces manual workload with automated workflows

Enables real‑time risk assessment and personalization

Improves accuracy, consistency, and speed across processes

Today’s top insurers are leveraging both predictive AI and generative AI — using machine learning not just for analytics but also for document automation, customer interaction, and knowledge extraction.

2. Cloud‑Native Platforms Power Agility and Integration

Legacy insurance systems often block innovation — slowing product launches, integration, and data flows. In 2026, leading U.S. carriers are replacing outdated infrastructure with cloud‑native, modular platforms. This transition enables faster deployments, better scalability, and seamless integration with partners, brokers, and embedded experiences.

Benefits include:

Faster product time‑to‑market

Lower infrastructure costs

Better resilience and disaster recovery

Cloud platforms also make it easier to connect with external ecosystems via APIs, supporting embedded insurance and real‑time data exchange.

3. Embedded Insurance and API‑First Tech Expand Reach

Customers today expect insurance when and where they need it. Embedded insurance — coverage offered directly through e‑commerce, travel platforms, mobility apps, and financial services — is now mainstream in the U.S. market.

What’s driving it:

API‑first systems that connect carriers with platforms in real time

Seamless purchase experiences at checkout

Higher adoption by consumers who prefer instant, digital options

This shift reflects broader embedded finance trends where insurance is part of the digital customer journey, not a separate purchase.

4. IoT and Telematics Enable Real‑Time Risk Intelligence

Connected devices and sensors — from vehicle telematics to smart home monitors and wearables — are transforming how risk is measured and priced. In 2026, insurers are using IoT to deliver usage‑based insurance (UBI) and proactive risk management.

Key use cases include:

Usage‑based auto insurance with safer driving incentives

Smart home risk alerts that reduce property claims

Wearable‑driven health and life insurance insights

IoT data helps shift insurance from reactive payouts to proactive prevention.

5. Parametric Insurance and Smart Contracts Bring Speed and Transparency

Parametric insurance — where payouts are triggered automatically by measurable events such as weather conditions — is gaining traction in the U.S. This model reduces complexity and speeds compensation, especially for climate‐linked risks.

Blockchain and smart contracts help power these solutions by automatically executing terms once specific conditions are met, improving transparency and reducing manual settlement steps.

6. Advanced Analytics and Big Data Improve Precision

Insurance companies now gather vast quantities of data — from telematics, social trends, satellite imagery, and more. Advanced analytics platforms make sense of this data, enabling:

More accurate pricing and risk scoring

Dynamic customer segmentation

Enhanced fraud detection

Predictive analytics is transforming everything from automation to personalization, making insurance both smarter and more customer‑centric.

7. Cybersecurity and Regulation‑Ready Tech

As insurers embrace digital platforms and AI, cybersecurity becomes critical. New technologies are emerging that protect sensitive customer data, secure APIs, and prevent breaches that could undermine trust or trigger regulatory penalties.

At the same time, regulatory tech (RegTech) is helping insurers manage compliance in an increasingly complex legal landscape.

What This Means for the U.S. Market in 2026

By 2026, technology has become insurance’s competitive engine. Insurers that embrace these innovations can:

✔ Deliver faster, more accurate underwriting

✔ Automate claims and reduce loss ratios

✔ Increase customer engagement with digital self‑service

✔ Expand distribution through embedded experiences

✔ Improve profitability with data‑driven pricing

U.S. carriers and insurtech startups that deploy these technologies strategically will define the next decade of insurance.

Conclusion

In 2026, the best insurance technology isn’t just about flashy features — it’s about integrating intelligence, agility, and real‑time insights into every part of the insurance lifecycle. From AI and cloud platforms to IoT, embedded insurance, and smart contracts, these technologies are reshaping how insurance is designed, sold, and serviced in the U.S. market.